Today, I too voted, exercising my constitutional and fundamental right to pick a party and a candidate of my choice.

My list of priorities apart from economic and social development is to choose a candidate and party who can uphold our constitutional rights of equality, secularism and liberty in letter and spirit and also ensure national security. The party that is given the mandate to govern for the next five years should have the vision to take India forward to a $ 10 Trillion economy, uplifting vast sections of the society and upholding the values enshrined in our constitution.

It was heartening to see the manifesto of both the major parties contain the roadmap to Economic growth for a $10 Trillion Indian economy, but it was disappointing to note that the lead players of both leading National parties were mostly silent on the most pressing economic issues during the campaign and run up to voting.

Even if political parties implement only 5% of all their promises, especially with regard to growth, jobs and social stability, they will be able to transform large sectors of India.

Slowing economic growth and lack of fiscal space to boost growth are going to be the main challenges for the new government. Boosting investment, especially private capex would be the key to ensure growth. For this, the government not only needs to provide ease of credit availability at viable rates but also improve sentiment and undertake key difficult reforms to ensure “Ease of business.”

Any country that has high interest rates, high land prices and high labour cost, cannot dream of achieving high single digit or double digit growth rates. For the Indian economy to achieve its true potential, the new government will have to address these basic issues on top priority.

Business has to be main priority if we want to revive economic growth and investments which have stagnated. We require rapid economic growth for job creation or we shall soon have our demographic advantage turning into social unrest.

In the years ahead, Disruption and change is going to be the only constant. Three primary forces are going to be driving this current wave of disruption: technology, globalization, and demographic change. Apart from other things, in today’s world, Disruption and change has resulted in reduced life cycle of most businesses.

Artificial intelligence and robotics are reinventing the workforce dynamics. Changing consumer preferences and expectations – most notably in the millennial generation – are altering consumption patterns and demand for everything from cars to real estate.

Advances in technology have been disrupting business models for centuries. In our lifetime, successive waves of the IT revolution, PC, online, mobile, social media, have democratized data, empowered consumers and spawned scores of new industries. The next waves – the Internet of Things (IoT), virtual reality, AI, robotics and God knows what else– promise to be even more revolutionary and disruptive.

Gig economy start-ups are already challenging regulations governing the operation of hotels, restaurants, taxis, E commerce and more. As the trend accelerates in the machine economy with advances in AI, Robotics etc, governments will need regulatory regimes designed for the future – nimble, real-time and powered by big data and smart technologies.

The march of disruption is unrelenting and this can leave today’s decision makers and leaders grappling with tremendous uncertainty and a broad array of challenges. Responding to disruption has become a central issue for incumbent organizations including the government, everywhere.

Are our institutions and the Government geared up to face this challenge?

More than money or tax cuts, what new-age companies certainly need is a less onerous regulatory culture that unshackles innovation and entrepreneurship.

The need of the time for all players whether the government or the businesses themselves is to be nimble footed, flexible and ultra responsive to change.

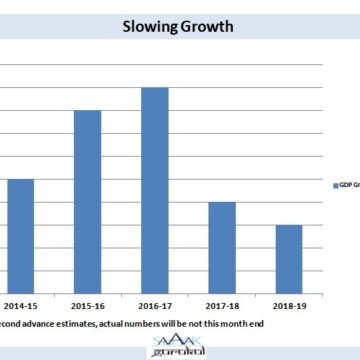

Apart from the above challenges, any new Government in India shall face several other immediate challenges so as to get the economy back on the rails. Leading economists fear that India may be stuck in Middle Income trap with growth rate stagnating at 5-6%.

In our more than seventy years since Independence, we have got political freedom, freedom of speech and all kinds of freedom to do what we want as citizens but unfortunately, we still have to get and enjoy Economic Freedom. The governments continues to control through various direct and indirect means our freedom to do business, to enter and exit businesses, to run businesses at optimum level and change businesses.

It is a tiny miracle that despite the high cost of capital, low productivity levels, lack of availability of skilled manpower, archaic controls on land use, excessive regulatory controls and low levels of automation and technology absorption, our country continues to be the fastest growing economy in the world.

Can you imagine the heights our economy will touch if the next government unshackles businesses; provide a more vibrant domestic venture capital system to tap the surplus overseas capital, reduce real interest rates, invest in human capital to create a productive workforce, rationalize land reforms to ensure land availability for Industry at viable rates, create a conducive environment for boosting innovation, entrepreneurship and startups, boost business confidence by ensuring clarity and continuity in Government policy and improve business sentiment.

I recently read a wonderful tweet by a leading CEO, “The best thing the new government can do for the business, is to let them do business.”

True indeed! The more the government tries to rope in and regularize businesses, the more obstacles it creates for itself and the growth of businesses; and mind you we are talking about legit, compliant and tax paying businesses. It tries to create conditions without fully understanding the dynamics of the business and the impact the controls can have beyond that business. Time and again we have seen that market forces alone can bring in controls and regulate the behaviour of respective businesses. We need a Government that stays away; Leave it to the business and let the business do business.

This is not to say that the government has no role to play and should not play in business. The best role the government can play is to create a conducive environment and regulatory framework to ensure the “Ease of Business.”

A strong economic revival package and right implementation of policies by the new government can help create as many as 150 million jobs in the next 10 years, the utmost need of the hour.

We have largely been dependent on a consumption led growth but now for the economy to grow in high single digits, it needs a boost in investment.

This cannot happen with government investment alone, it just does not have the funds or the fiscal prudence to bring in the kind of investment required.

Immediate steps need to be taken to address the issue of capital inadequacy. What the government needs to do is to create an environment and remove hurdles to tap the vast resources of capital available worldwide.

Government needs to make capital available for businesses at lower real rates. Consumer price inflation at less than 3% and a repo rate more than double that, is not the perfect recipe for capital investment.

India currently faces a major liquidity crisis. If global history is any guide, liquidity crisis not handled well can translate into a contagion and solvency crisis. NBFCs are facing acute stress due to asset liability mismatch. In corporate India, promoter entities with high leverage, are also facing stress. The real challenge for markets will be when liquidity risk intersects with default risk, which could then amplify credit risk into a downturn and have contagion effect. Policy makers need to act swiftly and ensure liquidity injection at reasonable rates to overcome the current crisis.

The new Government needs to build an eco system to nurture Start ups. It must remove regulatory hurdles, clear and bring consistency in tax matters, promote vibrant domestic venture funds and private equity culture. The solution lies in developing the Alternate Investment Fund (AIF) market, where we have patient capital with highly specialized skill-set. These funds can channelize a part of long-term savings with higher risk appetite into start ups.

To make efficient use of limited capital, we need to move up the value chain in terms of allocation of capital. It is about time that we move from “Make in India” to “Innovate in India”. The prime example in this case is of Apple which sources its products from China, India and the like at 10% of the selling price, and sells it back to them at a value addition of multiple times.

To ensure efficient use of available capital, government needs to exit from businesses not having any strategic interest and in loss making businesses which are becoming capital guzzlers and a constraint on government capital and finances.

Over the years, with improved digitalization, the access to credit has improved. But we still have a long way to go. India’s credit as (% of GDP) is low and financial system will need to deepen a lot more.

the government needs to ensure the allocation of available capital on purely economic factors to productive assets rather than misplaced priorities like “Cow Shelters” and the like.

Catalyze the financialization of household savings in India for a sustainable and stable liability side of banks, NBFCs, Mutual Funds, Pension Funds etc.

India’s wholesale funding market has not grown in line with the size of the economy. Refinancing options are not available for most lenders.

Structural reforms are immediately needed in the money market, corporate bond market space and also at the institutional level including banks, mutual funds, pension funds, insurance, auditors, NBFCs and rating agencies. Greater access should be given to the foreign investors who will bring in not only much needed capital but also best practices.

10) Steps need to be taken ti improve our tax to GDP and credit to GDP ratio which rank amongst the lowest in the world. No country can dream of sustainable Growth with such low level of compliance and disbursement ratios.

These above measures are just the beginning to address the economy’s structural problems. But, currently negative sentiments at the micro level is India’s most urgent economic problem. The government needs to boost the economy for a sentiment turnaround, after which the new government will be in a better position to address the more complex economic issues.

If nothing is done to quickly reverse sentiments, we would have lost a golden opportunity to reap the harvest of huge potential that our economy offers.

May the best man win. Here is wishing the new government support in its endeavour to take our country to greater heights. India’s youthful and aspirational population deserves a rapid transformation of the economy, which can deliver double-digit growth, jobs and prosperity to all.

Happy Investing!

Stay Blessed Forever

Sandeep Sahni

Note: All information provided in this blog is for educational purposes only and does not constitute any professional advice or service. Readers are requested to consult a financial advisor before investing as investments are subject to Market Risks.

About The author

Sandeep Sahni

Sandeep is an alum of IIM Lucknow with a Post Graduate Degree (MBA class of 1988). His also an alum of Shri Ram College of Commerce, Delhi University (B.Com. Hons. Class of 1985.)

Sandeep’s investing experience and study of the Financial Markets spans over 30 years. He is based in Chandigarh and has been advising more than 500 clients across the globe on Financial Planning and Wealth Management.

He has promoted “Sahayak Gurukul” which is an attempt to share thoughts and knowledge on aspects related to Personal Finance and Wealth Management. Sahayak Gurukul provides financial insights into the markets, economy and Investments. Whether you are new to the personal finance domain or a professional looking to make your money work for you, the Sahayak Gurukul blogs and workshops are curated to demystify investing, simplify complex personal finance topics and help investors make better decisions about their money.

Alongside, Sandeep conducts regular Investor Awareness Programs and workshops for Training of Mutual Fund Distributors, and workshops and seminars on Financial Planning for Corporate groups, Teachers, Doctors and Other professionals.

Through his interactions and workshops, Sandeep works towards breaking the myths and illusions about money and finance.

He also writes a well read blog;

He has also conducted presentations, workshops and guest lectures at Management institutes for students on Financial Planning and Wealth Creation.

He can be reached at:

+91-9888220088, 9814112988

sandeepsahni@sahayakassociates.com

Follow us on:

www.facebook.com/sahayakassociates

www.twitter.com/sahayakassociat,https://www.instagram.com/sahayakassociates